What did we learn this year? Well, not too much. Observing is not learning. Acting is. But we’re not going to do that. A call for action is sufficient, as long as someone else does it. That much we’ve learned. Pandemic Time What used to take several years now takes a fraction of that –…

Financial markets are imbalanced and lack liquidity in crucial sectors, even historically stable and predictable markets such as the global bond and currency markets. Investments are slanted in one direction more frequently and the markets are vulnerable to big price swings as a result. These large global markets are not immune to ever more lopsided trades creating extreme volatility. This occurs even when a small change occurs in positions, sentiment, or news. Even the world’s most liquid markets, US dollar currency trades and US Treasuries, are seeing skewed positioning resulting in surprisingly large shifts in prices and Treasury bond yields.

The market now leans too far one way or the other, and that imbalance will be forced to reverse more powerfully and unpredictably.

Transformation, Valuation, Employment, and Deflation

Disruption to some of the world’s most important industries, deflationary pressure caused by scaling lower-cost businesses, and sustained low interest rates challenge traditional valuation models. Technological platforms, from blockchain-based businesses to energy storage to DNA sequencing, enable unprecedented disruption to business and economic models.

Interest rates will remain low, equity values will remain high, innovation will drive deflationary pressure, and volatility will be intense and frequent. A new approach is required to understand dynamic global competition and sustainable value.

There are warning signs that the stock market is transitioning from some form of reality to misguided euphoria. The S&P 500 is up almost 10% in the last 30 days. However, this broad optimism doesn’t seem to be matched by many forms of fundamental reality.

Earnings are barely moving, and profit margins are under pressure from higher wages and rising product costs. However transitory one imagines supply chain constraints and lack of available workers, the situation has certainly extended much further than most predicted.

Distinguishing what’s happening in the market and the direction of important market metrics – the signal – from garbled, inconsistent, and mostly useless data – the noise – is extremely challenging today. Information is contradictory and transient making data and critical events more confusing and indistinguishable. Unusual circumstances brought about by the pandemic, subsequent supply chain interruptions, inconsistent production and demand, and unclear economic forecasts combined for almost unprecedented uncertainty and unpredictability.

Typically, near-term predictions are reasonable and reliable because we have immediately available and fairly accurate data making short-term predictions reasonably accurate. In other words, we can estimate what will happen because we have a good idea what just happened. But this is not the case today. Predictions based on the near-term past are more muddled now than ever. While we used to be able to say we can see a trend, whether that’s inflation, economic growth, or some other important metric, too much volatility, irrelevance, and lack of applicability (after all, who is going to project from a base that includes a pandemic impacting global supply chains and production?), we really can’t reasonably rely on any of that data to try to find a trend or connect the dots generating a near-term forecast with any meaningful depth of data and understanding

More intense volatility occurring more often will be characteristic of this market from now on. An investment strategy must withstand and profit from this. The only clear signal from the market is that there is far too much noise and not enough of a clear signal. Without clarity, determining an investment strategy is flying blind with no instruments.

Core holdings combined with an ability to withstand and profit from volatility and unpredictability are essential for investors today.

Assume nothing, new models and analytical tools, coupled with constant revision, questioning everything, reassessing, and re-analyzing, are essential to success in today’s markets. Often, and we are seeing that in today’s market, relying on bad assumptions, dogma, or prior belief can be disastrous.

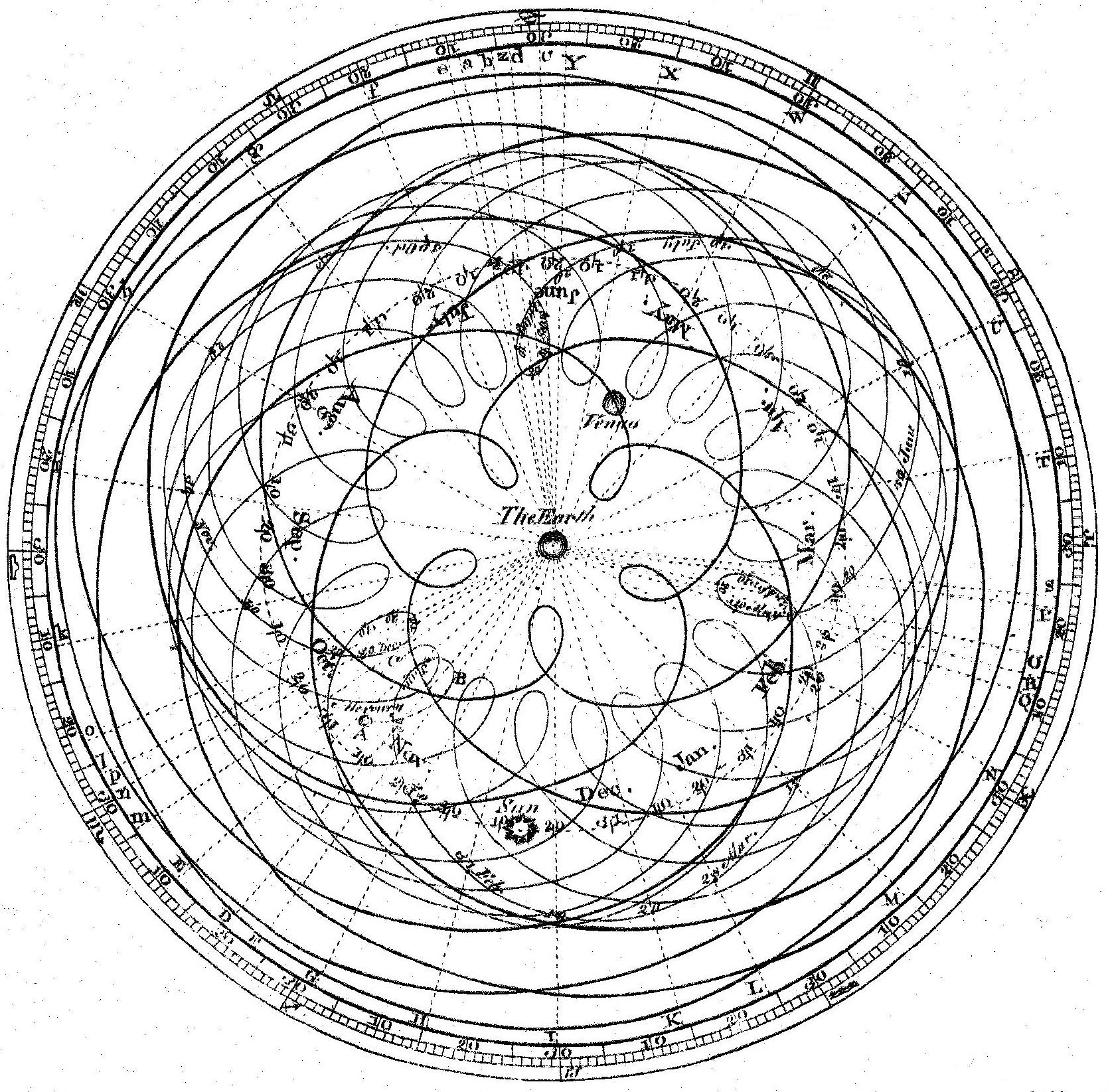

This story about medieval astronomy applies directly to investment strategies, market valuations, and portfolio construction today. It’s the same lesson –begin by questioning the very assumptions on which an entire system is built. There is also a very specific application of this model that is particularly current.

One of the most valuable lessons is to assume no knowledge and analyze closely every initial assumption. Nothing is so obvious that it can’t be questioned. Unexamined ideas and assumptions will eventually be useless. Any assumptions and any model used to explain and predict anything (whether it’s the movement of planets or financial markets) needs to go back to first principles and discard any assumptions, preconceived knowledge, or bias.

Economic predictions have always been highly variable and uncertain, and, for some reason, relied upon as if the future were a magical algorithm. Essentially, economists would make one fundamental mistake. They thought they were practicing a science. Data could be collected, inputted, and a predictive algorithm could be generated. Even Nobel Prize winners like Paul Samuelson believed that with enough data we could come to understand the economy and how it functioned.

This is nonsense. As Daniel Kahneman and Amos Tversky have shown us, human behavior and irrationality, combined with unpredictability and randomness (thank you Naseem Taleb) make this even a questionable social science. Using existing analysis and algorithms to reliably forecast is a fool’s errand, essential for someone’s tenure, and maybe even a Nobel Prize, but doesn’t add much that is useful. Some of the more laughable Nobel Prizes have been given to people who determined that markets were efficient. They are not. Economies can be predicted with useful data input. They cannot. A couple of inputs about inflation and the unemployment rate, and we know how to manage an economy. We can’t. That last one is the Philip’s Curve – true for a limited time and then it goes spectacularly wrong – a lot like most risk and market prediction models.