Risk is higher. Markets are more unpredictable, and valuations more volatile. So, when anyone says “this time it’s different” it usually makes good sense to stop listening. However, these days the markets have given us more frequent and intense volatility. The NASDAQ is down almost 30% so far this year, and shocks from the pandemic, the Ukrainian war, massive central bank interest-rate maneuvers, and China’s zero-covid policy, are all ongoing inputs for turmoil that will continue for some time. Persistent uncertainty creates higher costs of capital and less affordability, weakening business investment, slowing GDP growth, and reducing investment returns. Hyperbolic “this time it’s different” statements are turning out to be true. This time days look darker, uncertainty greater, economic growth lower, vulnerability to additional shocks higher, and investors fear many more dark days to come. More frequent and intense volatility will not be calmed anytime soon. It really may be different this time.

While most of Europe and the United States suffer sweltering heat, darkening economic skies and bitter winter of discontent are looming. Threats to the world economy are chilling. Rising interest rates are slowing activity for discretionary spending while rising prices for nondiscretionary spending are also slowing economic activity. It would be miraculous if the compounding of both effects would not lead to a recession in both Europe and the US. China’s growth has stalled. The Ukraine conflict will resolve itself to the West’s dramatic disadvantage and the West seems to be willing to let it happen – much to each economy’s long-term disadvantage. Don’t count on anything miraculous.

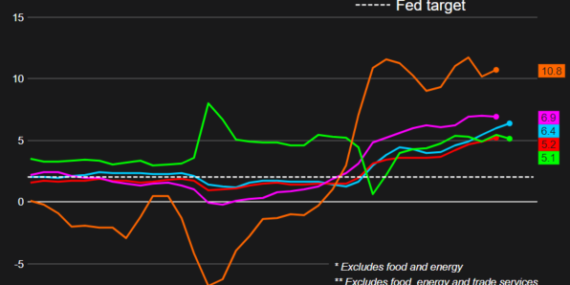

The average prices of food and fuel rose more than 16% in February from a year earlier and are expected to rise further by the war in Ukraine. Consumers are paying much more for meat, bread, milk, shelter, gas, and utilities. Only a small amount of food consumed in the U.S. is imported, and most of that is from Mexico and Canada. But Russia provides 15% of the world’s fertilizer and other agricultural chemicals that are now in short supply as planting season approaches. Wheat futures are up 29% since Feb. 25 and corn is up 15%. There is no shortage of wheat in the U.S., but global supply was the tightest in 14 years before the conflict, and dramatic shortages and price spikes are expected. What data is the Fed looking at, and how is it assessing inflationary risks? It’s hard to feel confident that the right hands are on the wheel because the combination of extraordinary factors, such as extremely tight labor markets and wage inflation (at over 6% annually and accelerating) showed inflation was already a significant risk. Yet interest rates were left unaltered. This is even before the crisis in Ukraine. The Fed should do whatever is necessary with interest rates to bring down inflation, including movements of more than a quarter-point, and a rapid reduction of its balance sheet. It also means recognizing that unemployment is likely to rise over the next couple of years. Paul Volcker would not have had to take extraordinary steps, driving the economy into a recession to crush runaway inflation, if his predecessors had not lost their focus on inflation. To avoid stagflation and the associated loss of public confidence in our economy today, the Fed has to do more than merely adjust its policy dials — it will have to head in a dramatically different direction.

Distinguishing what’s happening in the market and the direction of important market metrics – the signal – from garbled, inconsistent, and mostly useless data – the noise – is extremely challenging today. Information is contradictory and transient making data and critical events more confusing and indistinguishable. Unusual circumstances brought about by the pandemic, subsequent supply chain interruptions, inconsistent production and demand, and unclear economic forecasts combined for almost unprecedented uncertainty and unpredictability.

Typically, near-term predictions are reasonable and reliable because we have immediately available and fairly accurate data making short-term predictions reasonably accurate. In other words, we can estimate what will happen because we have a good idea what just happened. But this is not the case today. Predictions based on the near-term past are more muddled now than ever. While we used to be able to say we can see a trend, whether that’s inflation, economic growth, or some other important metric, too much volatility, irrelevance, and lack of applicability (after all, who is going to project from a base that includes a pandemic impacting global supply chains and production?), we really can’t reasonably rely on any of that data to try to find a trend or connect the dots generating a near-term forecast with any meaningful depth of data and understanding

More intense volatility occurring more often will be characteristic of this market from now on. An investment strategy must withstand and profit from this. The only clear signal from the market is that there is far too much noise and not enough of a clear signal. Without clarity, determining an investment strategy is flying blind with no instruments.

Core holdings combined with an ability to withstand and profit from volatility and unpredictability are essential for investors today.

Separating signal versus noise is challenging these days because today’s signal is more muddled than ever. One of the more unusual circumstances, which I covered in more detail in the article “Important and Unknowable” is that the immediate past is telling us extraordinarily little about the near future. That is unusual because we can typically…

We are rapidly approaching a zero-interest rate world. In the face of the dramatic negative impact of the pandemic, as well as existing and lingering economic fallout, central banks’ interest rate toolbox will be empty soon. The only remaining weapon will be fiscal policy. Among other things, fiscal policy and domestic financial markets will have an overwhelming influence on global currencies.

Productivity, expansion, and entrepreneurship were enabled through the adoption of new technology. Undeniably, the net economic benefit was substantial. But lives were disrupted, jobs were lost, and what would be seen with a historical perspective as an obvious beneficial choice, was anything but obvious to those so immediately and negatively impacted.

Technological advancements produce net benefits for society. But for every advancement, there is a cost. Leadership and subsequent public policy must address this shortfall. As in the past, the solution has been training and education leading to economic inclusion and prosperous lives.

History has taught us the net benefit of technological advancement, the turmoil it brings, and the solution required.

Chinese economic policies and motivations since 2008 not only emphasize growth and sustainability of state-owned enterprises but, a critical but much less well-appreciated dimension is the Chinese government’s emphasis on stability. No economic policy in China will ignore this, and the high value placed on stability pervades all the current trade talks with the United…