A new vision for artificial intelligence is using smaller more relevant data sets for dynamic learning generating more effective outcomes and better predictions. This model uses cognitive architecture, learns, transfers learning, and retains knowledge – enabling more valuable and compelling artificial intelligence applications. This approach is more closely related to the brain’s actual structures and much more effective than “neural networks,” which is a catchy name but the similarity to the brain’s actual functioning is in name only. Real advancement in artificial intelligence must live in reality, not theoretical marketing. The current state of artificial intelligence shows the shortcomings of big data and trial-and-error approaches. A new AI vision can be a more effective solution. Smaller data sets, more relevant information, dynamic data, and algorithms will lead to more appropriate outcomes, better tools, and more effective applications.

Predictions usually end up being nonsense. We simply draw a trajectory from what we know today. But innovation is a discontinuity. Things are unpredictable because innovation does not come from consensus thinking. It comes from small groups and individuals with a spark of entrepreneurship, intelligence, and vision.

One of the fundamental tenets of predicting technology is that most forecasters get things spectacularly wrong.

The illusion that one can either predict or get ahead of cycles, or predict when they will end is why most investors underperform the market. Markets are driven by human emotion, and it is human emotion combined with the supply and demand dynamic that determines price. Therefore, pricing is independent of anyone’s perspective about “intrinsic value.” Markets are based on price, price is based on supply and demand, and that dynamic is subject to abrupt changes based on the whims of small numbers, and sometimes exceptionally large numbers, of investors. Human behavior controls the markets. Optimism, pessimism, psychology, fear, conviction, and resignation all play a role in adding to volatility and uncertainty. Frequent and intense volatility is here to stay. Market movements really can’t be predicted unless they are at extremes when prices are at absurd highs or lows. But, picking the high or the low is a fool’s errand. Understanding and profiting from volatility, managing risk, and believing in a sustainable investment model is still the best strategy.

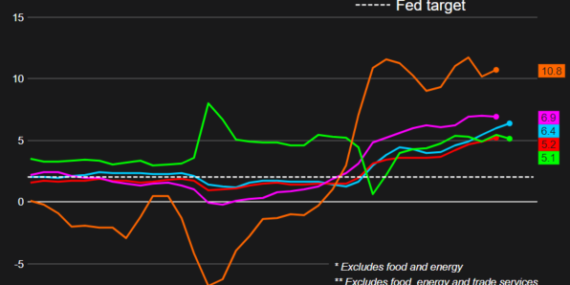

The average prices of food and fuel rose more than 16% in February from a year earlier and are expected to rise further by the war in Ukraine. Consumers are paying much more for meat, bread, milk, shelter, gas, and utilities. Only a small amount of food consumed in the U.S. is imported, and most of that is from Mexico and Canada. But Russia provides 15% of the world’s fertilizer and other agricultural chemicals that are now in short supply as planting season approaches. Wheat futures are up 29% since Feb. 25 and corn is up 15%. There is no shortage of wheat in the U.S., but global supply was the tightest in 14 years before the conflict, and dramatic shortages and price spikes are expected. What data is the Fed looking at, and how is it assessing inflationary risks? It’s hard to feel confident that the right hands are on the wheel because the combination of extraordinary factors, such as extremely tight labor markets and wage inflation (at over 6% annually and accelerating) showed inflation was already a significant risk. Yet interest rates were left unaltered. This is even before the crisis in Ukraine. The Fed should do whatever is necessary with interest rates to bring down inflation, including movements of more than a quarter-point, and a rapid reduction of its balance sheet. It also means recognizing that unemployment is likely to rise over the next couple of years. Paul Volcker would not have had to take extraordinary steps, driving the economy into a recession to crush runaway inflation, if his predecessors had not lost their focus on inflation. To avoid stagflation and the associated loss of public confidence in our economy today, the Fed has to do more than merely adjust its policy dials — it will have to head in a dramatically different direction.

Distinguishing what’s happening in the market and the direction of important market metrics – the signal – from garbled, inconsistent, and mostly useless data – the noise – is extremely challenging today. Information is contradictory and transient making data and critical events more confusing and indistinguishable. Unusual circumstances brought about by the pandemic, subsequent supply chain interruptions, inconsistent production and demand, and unclear economic forecasts combined for almost unprecedented uncertainty and unpredictability.

Typically, near-term predictions are reasonable and reliable because we have immediately available and fairly accurate data making short-term predictions reasonably accurate. In other words, we can estimate what will happen because we have a good idea what just happened. But this is not the case today. Predictions based on the near-term past are more muddled now than ever. While we used to be able to say we can see a trend, whether that’s inflation, economic growth, or some other important metric, too much volatility, irrelevance, and lack of applicability (after all, who is going to project from a base that includes a pandemic impacting global supply chains and production?), we really can’t reasonably rely on any of that data to try to find a trend or connect the dots generating a near-term forecast with any meaningful depth of data and understanding

More intense volatility occurring more often will be characteristic of this market from now on. An investment strategy must withstand and profit from this. The only clear signal from the market is that there is far too much noise and not enough of a clear signal. Without clarity, determining an investment strategy is flying blind with no instruments.

Core holdings combined with an ability to withstand and profit from volatility and unpredictability are essential for investors today.

Separating signal versus noise is challenging these days because today’s signal is more muddled than ever. One of the more unusual circumstances, which I covered in more detail in the article “Important and Unknowable” is that the immediate past is telling us extraordinarily little about the near future. That is unusual because we can typically…

Economic predictions have always been highly variable and uncertain, and, for some reason, relied upon as if the future were a magical algorithm. Essentially, economists would make one fundamental mistake. They thought they were practicing a science. Data could be collected, inputted, and a predictive algorithm could be generated. Even Nobel Prize winners like Paul Samuelson believed that with enough data we could come to understand the economy and how it functioned.

This is nonsense. As Daniel Kahneman and Amos Tversky have shown us, human behavior and irrationality, combined with unpredictability and randomness (thank you Naseem Taleb) make this even a questionable social science. Using existing analysis and algorithms to reliably forecast is a fool’s errand, essential for someone’s tenure, and maybe even a Nobel Prize, but doesn’t add much that is useful. Some of the more laughable Nobel Prizes have been given to people who determined that markets were efficient. They are not. Economies can be predicted with useful data input. They cannot. A couple of inputs about inflation and the unemployment rate, and we know how to manage an economy. We can’t. That last one is the Philip’s Curve – true for a limited time and then it goes spectacularly wrong – a lot like most risk and market prediction models.

Clear and coherent markets, free from political agenda, bad compromises, and ineffective regulation is almost nonexistent. The consequences are usually pyrotechnic. It is not as if the world hadn’t provided ample warnings about the risks associated with irresponsible finance. History has centuries worth of such examples, but even looking at recent events over the last 25 years is illuminating.

In spite of Alan Greenspan acknowledging the “irrational exuberance” of the markets in 1996, stock market valuations continued to rise. The warning signs of unstable economies were believed to be localized and the broader markets decoupled from this turbulence. This was naïve thinking then and outright irresponsible now.

The idea that markets are uncertain, and consistent prediction is essentially impossible, is not new. John Maynard Keynes published a book on probability and uncertainty in 1921, with this concept of uncertain and irrational markets forming the basis of his general theory of financial markets. So, years before the stock market crash of 1929, and almost every 10 to 15 years afterward, the cycle of financial crashes and panics was predicted by a well-publicized thinker, and then, as is typical, ignored. The lesson is simple, and Keynes laid it out 100 years ago: markets seem rational but only during periods of stability. Markets are uncertain. Predictive models work most of the time, and that is their fundamental flaw. They will fail. Investment models that account for uncertainty and failure succeed in the long term.

The world economy is an infinitely complicated web of interconnections. We each experience a series of direct economic interrelationships: the stores we buy from, the employer that pays us our salary, the bank that gives us a home loan, etc. But once we are two or three levels degrees separated, it’s impossible to really know with any confidence how the connections are working. That, in turn, shows what is unnerving about the economic calamity potentially accompanying the coronavirus.

In the years ahead we will learn what happens when that web is torn apart when millions of those links are destroyed all at once. It opens the possibility of a global economy quite different from the one that has prevailed in recent decades. Or, as John Kenneth Galbraith has said, “we have two classes of forecasters: those who don’t know and those who don’t know they don’t know. “The bottom line is establishing and maintaining an unconventional investment profile requires acceptance of uncomfortably idiosyncratic portfolios, which frequently appear imprudent in the eyes of conventional wisdom. We are entering a new world and must think differently.