The government is providing a backstop for all government-backed securities. The Fed is also going to be extremely active in the markets, buying not only fixed-income securities but also stock index funds. They are working very hard to keep the market aloft and preventing it from cratering (they still may not be successful). This is an election year and this administration will do everything it can to make sure things look as good as possible through November.

I understand there is riskiness, but I expect economic activity and fed support to continue to increase. Even if we have an increase in coronavirus cases, people will remain optimistic – justifiably or not.

There will be extreme volatility. Economic activity will waiver, increase suddenly, pull back, and the pattern will continue for some time to come.

Market volatility is our friend because we have a stable source of cash flow that protects our capital base. On top of that, the speculative strategy will profit from volatility while the equity investment strategy will play for the long term – it is a multi-year long-term perspective.

Although there are a handful of investments where confidence in the five-year curve is justified, and now is a great time to make these long-term investments, it is still very unpredictable.

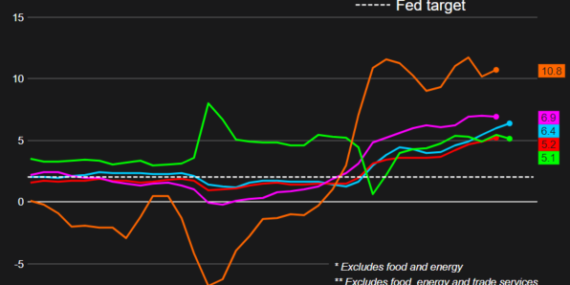

The short- and long-term state of the economy, how this massive amount of debt gets repaid, how we reopen businesses, etc. is unknown, volatile, and any attempt to predict seems fruitless. But, understanding how to adjust for risk, accept, and ultimately take advantage of volatility, will be powerful. Along with a long-term perspective, this will be the most effective investment strategy. The Fed is printing more money. We’re going to see a lot of capital injected into the global economy. But the presence of money is not the important factor. It’s the velocity of money – how people are spending it and is that money chasing after other goods. That will drive inflation. We didn’t see it in the past even though we had a massive capital injection. Deflation and recession are much bigger concerns. Inflation is not on the horizon. The Fed’s enhanced bond-buying, which includes high-yield bonds and other fixed-income securities is unprecedented and has boosted the value of debt portfolios. However, these portfolios (mostly just above or just below investment grade) still yield attractive disproportionate risk-adjusted returns.