There are warning signs that the stock market is transitioning from some form of reality to misguided euphoria. The S&P 500 is up almost 10% in the last 30 days. However, this broad optimism doesn’t seem to be matched by many forms of fundamental reality.

Earnings are barely moving, and profit margins are under pressure from higher wages and rising product costs. However transitory one imagines supply chain constraints and lack of available workers, the situation has certainly extended much further than most predicted.

Central bank independence and fiscal responsibility matter, even though the Western world is acting as if these rules no longer apply. Well, perhaps. But the world has given us three examples where the consequences are extreme when these basic foundations of economic policy are ignored or violated.

Decentralized finance (DeFi) can disrupt global finance – but only if Defi systems and central governments cooperate. Yes, sworn enemies cooperating for the greater good.

While each seems to be the sworn enemy of the other, ultimately, a cooperative relationship between decentralized and efficient (versus anachronistic and cumbersome) financial infrastructure and government central banks with stable currencies is absolutely necessary.

Defi transactions, to scale globally, require stable and predictable value. Government-issued currencies are the only reliable and foreseeable foundation. Cryptocurrencies, such as Bitcoin were never currencies. They are a sideshow that will remain a speculative asset, and increasingly unimportant.

Cryptocurrencies represent an architectural shift in how financial infrastructure and technology interact, and therefore, it is disrupting how the financial industry works globally. It is neither a new kind of money system nor a danger to economic stability. It is more important than that.

Investors have been swept up in the notion of “philanthropic capitalism” and have targeted life-sciences as an avenue that can fulfill this benefit to society. While laudable in concept, this is non-scientific surrealism. “Hoped-for” is not a reliable business model, and most of the unrealistic goals would not be sustainable even if achieved. Real science and innovation are more impactful and substantial and make life sciences even more.

Distinguishing what’s happening in the market and the direction of important market metrics – the signal – from garbled, inconsistent, and mostly useless data – the noise – is extremely challenging today. Information is contradictory and transient making data and critical events more confusing and indistinguishable. Unusual circumstances brought about by the pandemic, subsequent supply chain interruptions, inconsistent production and demand, and unclear economic forecasts combined for almost unprecedented uncertainty and unpredictability.

Typically, near-term predictions are reasonable and reliable because we have immediately available and fairly accurate data making short-term predictions reasonably accurate. In other words, we can estimate what will happen because we have a good idea what just happened. But this is not the case today. Predictions based on the near-term past are more muddled now than ever. While we used to be able to say we can see a trend, whether that’s inflation, economic growth, or some other important metric, too much volatility, irrelevance, and lack of applicability (after all, who is going to project from a base that includes a pandemic impacting global supply chains and production?), we really can’t reasonably rely on any of that data to try to find a trend or connect the dots generating a near-term forecast with any meaningful depth of data and understanding

More intense volatility occurring more often will be characteristic of this market from now on. An investment strategy must withstand and profit from this. The only clear signal from the market is that there is far too much noise and not enough of a clear signal. Without clarity, determining an investment strategy is flying blind with no instruments.

Core holdings combined with an ability to withstand and profit from volatility and unpredictability are essential for investors today.

Assume nothing, new models and analytical tools, coupled with constant revision, questioning everything, reassessing, and re-analyzing, are essential to success in today’s markets. Often, and we are seeing that in today’s market, relying on bad assumptions, dogma, or prior belief can be disastrous.

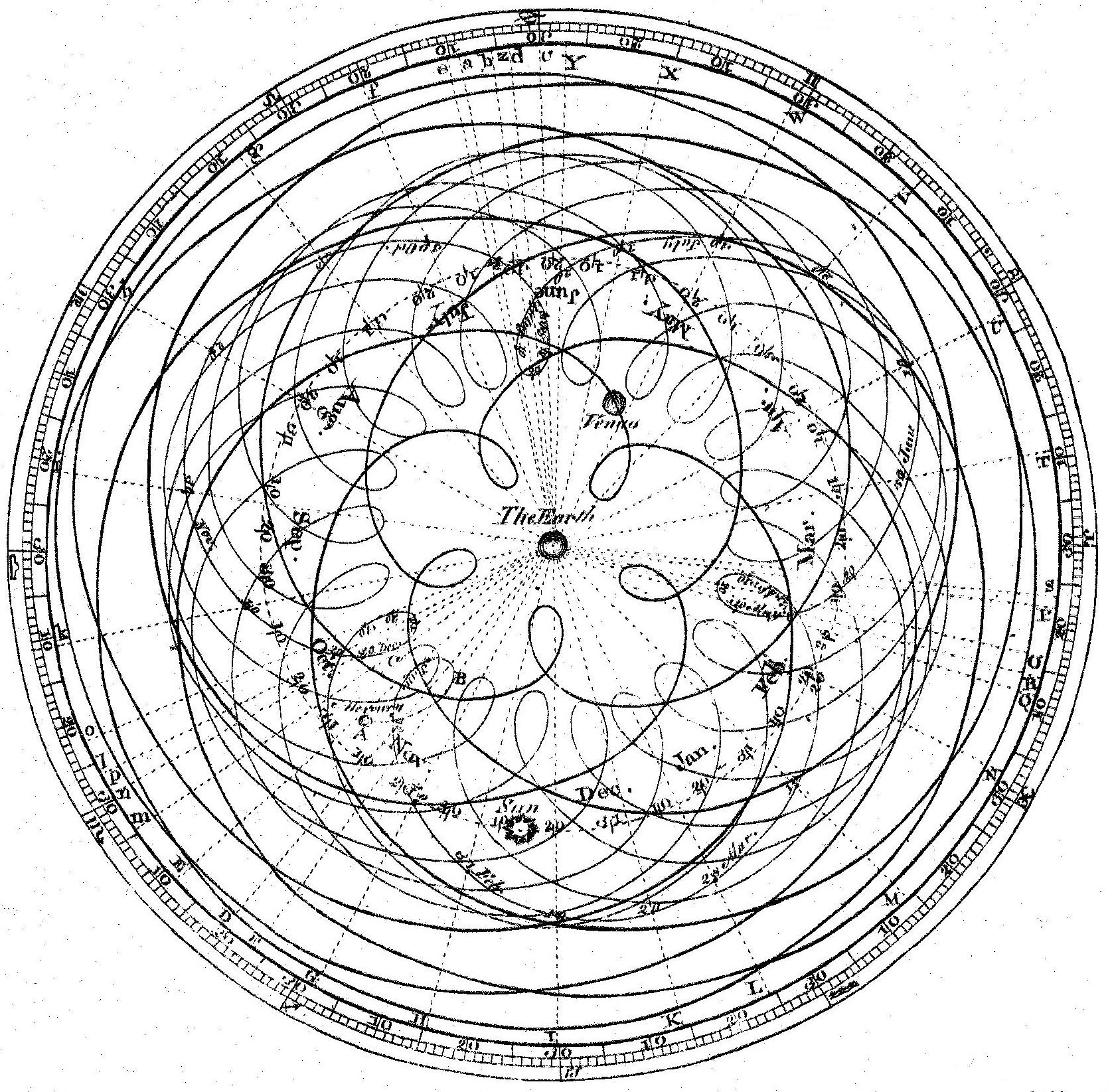

This story about medieval astronomy applies directly to investment strategies, market valuations, and portfolio construction today. It’s the same lesson –begin by questioning the very assumptions on which an entire system is built. There is also a very specific application of this model that is particularly current.

One of the most valuable lessons is to assume no knowledge and analyze closely every initial assumption. Nothing is so obvious that it can’t be questioned. Unexamined ideas and assumptions will eventually be useless. Any assumptions and any model used to explain and predict anything (whether it’s the movement of planets or financial markets) needs to go back to first principles and discard any assumptions, preconceived knowledge, or bias.

Technology is facing a substantial crossroads as policy changes with global resonance, such as China’s new crackdown on the country’s big tech companies (such as Ant Financial and Didi Global), the rising resistance to social media behemoths like Facebook, and the need for governments, whether in the United States, Western Europe, or China, to manage and control technological development. Regardless of any good intentions, this will add friction, inefficiency, and underperformance to the most dynamic global industry. The best intentions usually bring disastrous consequences. China cannot escape the law of unintended consequences. Trying to “manage” innovation and creativity takes away the often unplanned and serendipitous breakthroughs that make many significant advancements possible in the first place. From an economic perspective, capital is not going to invest in an uncertain environment where prosperity is managed and, despite great risk where most ventures will fail, the truly successful ones which make up for the losses and encourage capital to keep investing, will be mitigated. The vanguard of capital flight from China is beginning, and it will not ease if this policy and attitude are not revised. This attempt at “fairness and more equal distribution” will do nothing more than keep capital away and stifle any attempt at creativity, technical innovation, and economic advancement. The intention of this policy will yield the opposite outcome as a consequence. The signal means substance. Substance means innovation, creativity, and competitive dynamics that create the most effective innovations, the best solutions, and the most sustainable companies. Central planning, bureaucratic industrial policy, government-led economic management, and dictatorial focus have always failed, and always will. The US should not fall into this trap, regardless of how appealing it may be.

Economic predictions have always been highly variable and uncertain, and, for some reason, relied upon as if the future were a magical algorithm. Essentially, economists would make one fundamental mistake. They thought they were practicing a science. Data could be collected, inputted, and a predictive algorithm could be generated. Even Nobel Prize winners like Paul Samuelson believed that with enough data we could come to understand the economy and how it functioned.

This is nonsense. As Daniel Kahneman and Amos Tversky have shown us, human behavior and irrationality, combined with unpredictability and randomness (thank you Naseem Taleb) make this even a questionable social science. Using existing analysis and algorithms to reliably forecast is a fool’s errand, essential for someone’s tenure, and maybe even a Nobel Prize, but doesn’t add much that is useful. Some of the more laughable Nobel Prizes have been given to people who determined that markets were efficient. They are not. Economies can be predicted with useful data input. They cannot. A couple of inputs about inflation and the unemployment rate, and we know how to manage an economy. We can’t. That last one is the Philip’s Curve – true for a limited time and then it goes spectacularly wrong – a lot like most risk and market prediction models.

Fundamental drivers for pricing valuations in public markets have changed. Now, there is a new interaction among factors unseen just recently. Advanced technologies such as artificial intelligence have had a profound impact on the tools available and analysis presented to even the most amateurish investor. Social media, such as Reddit, Twitter, and other platforms, have allowed access to information and influence from media “stars” driving demand in an almost herd-like mentality driving up prices, and causing extreme volatility. Finally, technology has enabled a trading floor to be in everyone’s pocket. That same trading floor allows access to any information on anything from anywhere, and communication with anyone or, via social media, receive communication and information (regardless of how dubious) from anyone about any security or investment strategy.

These factors will cause unprecedented market volatility, along with extreme price movements for well-known (or perhaps more accurately, well-publicized) companies and their securities. While the supply of securities remains somewhat constant, demand for those securities is increasing (sometimes exponentially) because many more investors are now chasing those same securities.

The price of anything cannot escape supply and demand dynamics. Recent IPO activity is an attempt to meet growing demand (and raise capital at attractive prices). The new supply from IPO’s, secondary stock issuances, and most recently and monumentally, SPAC offerings, still do not provide enough supply to quench a growing and overwhelming demand. The valuations, especially those given to the SPAC’s, are entering stratospheric levels that could hardly be justified under normal market conditions. Successful investors are the ones who understand adding return without corresponding risk is the most critical component of successful investing, especially given the new equation for valuation:

Economics + Advanced Technologies + Social Media = Price

These three components are now inexorably linked and constitute an influential role in determining valuation from now on.

The More Things Change…

The pandemic has challenged many preconceived notions about the economy, markets, and public policy – and has impacted the way we live. But the inescapable truth remains unchanged:

There is no magic answer. No solution other than superior skill enables an investor to earn a high return safely and dependably. That is even more true in today’s low-interest rate, low return Tower of Babel world.

The world economy is an infinitely complicated web of interconnections. We each experience a series of direct economic interrelationships: the stores we buy from, the employer that pays us our salary, the bank that gives us a home loan, etc. But once we are two or three levels degrees separated, it’s impossible to really know with any confidence how the connections are working. That, in turn, shows what is unnerving about the economic calamity potentially accompanying the coronavirus.

In the years ahead we will learn what happens when that web is torn apart when millions of those links are destroyed all at once. It opens the possibility of a global economy quite different from the one that has prevailed in recent decades. Or, as John Kenneth Galbraith has said, “we have two classes of forecasters: those who don’t know and those who don’t know they don’t know. “The bottom line is establishing and maintaining an unconventional investment profile requires acceptance of uncomfortably idiosyncratic portfolios, which frequently appear imprudent in the eyes of conventional wisdom. We are entering a new world and must think differently.