Folly and the Fed

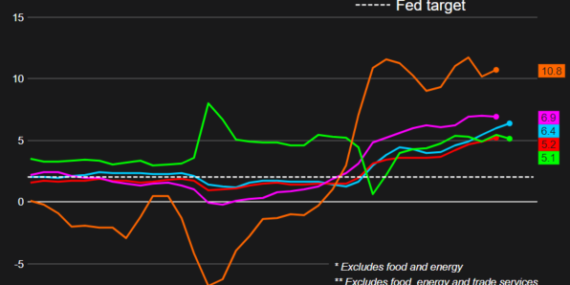

The average prices of food and fuel rose more than 16% in February from a year earlier and are expected to rise further by the war in Ukraine. Consumers are paying much more for meat, bread, milk, shelter, gas, and utilities. Only a small amount of food consumed in the U.S. is imported, and most of that is from Mexico and Canada. But Russia provides 15% of the world’s fertilizer and other agricultural chemicals that are now in short supply as planting season approaches. Wheat futures are up 29% since Feb. 25 and corn is up 15%. There is no shortage of wheat in the U.S., but global supply was the tightest in 14 years before the conflict, and dramatic shortages and price spikes are expected. What data is the Fed looking at, and how is it assessing inflationary risks? It’s hard to feel confident that the right hands are on the wheel because the combination of extraordinary factors, such as extremely tight labor markets and wage inflation (at over 6% annually and accelerating) showed inflation was already a significant risk. Yet interest rates were left unaltered. This is even before the crisis in Ukraine. The Fed should do whatever is necessary with interest rates to bring down inflation, including movements of more than a quarter-point, and a rapid reduction of its balance sheet. It also means recognizing that unemployment is likely to rise over the next couple of years. Paul Volcker would not have had to take extraordinary steps, driving the economy into a recession to crush runaway inflation, if his predecessors had not lost their focus on inflation. To avoid stagflation and the associated loss of public confidence in our economy today, the Fed has to do more than merely adjust its policy dials — it will have to head in a dramatically different direction.